Table of Content

- Rocket Mortgage

- Withdrawal for Home Purchase

- Find ways to increase your income instead of using 401k withdrawals for your home purchase

- What reasons can you withdraw from a 401(k) without penalty?

- Find out how much you need to save

- Save instead of using 401k withdrawals for a home purchase

- How To Use Your 401(k) To Buy a House?

This site is not authorized by the New York State Department of Financial Services. No mortgage applications for properties located in the state of New York will be accepted through this site. Deciding to withdraw from a 401 will mean taking a good look at your financial situation. We analyze and compare tools to help you make the best decisions for your personal financial situation. You know you’ve always wondered how much a partridge in a pear tree costs.

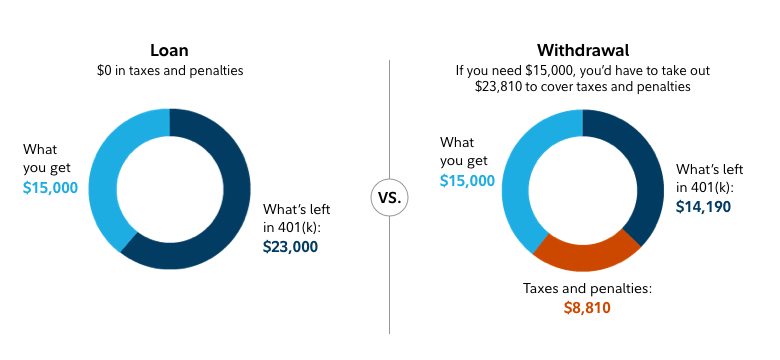

If they don’t—or if you need more than a $50,000 loan—then you might consider an outright withdrawal from the account. With this strategy, you will incur a 10% penalty on the amount you withdraw from a traditional 401 unless you meet requirements for an exemption. If you need more than $50,000 or your 401 provider does not allow loans, then you will need to make a withdrawal.

Rocket Mortgage

Qualifying for such exemptions is difficult by design, however. If you possess other assets that could be used for your home purchase, then you likely won’t qualify for an exemption. Even if you do, your withdrawal will still be taxed as income. Many first-time home buyers have some type of debt to worry about.

Based on the information you have provided, you are eligible to continue your home loan process online with Rocket Mortgage. If you do decide to use your 401 to buy a home, there are two options available. Find AgentsIf you don't love your Clever partner agent, you can request to meet with another, or shake hands and go a different direction.

Withdrawal for Home Purchase

Maybe you lost your job and are trying to make ends meet or you had to use your savings on a medical emergency. There is one option; it is called the 401K hardship withdrawal. If you get fired, laid off, or leave your job before you pay off the loan, you’ll have to pay the balance in full before the federal tax deadline the following year .

In withdrawing from your 401k, you’ll have to pay income tax on the withdrawals and if you’re under 59 ½, you’ll incur a 10% penalty on the withdrawn funds. Under these provisions, first-time home buyers are allowed to withdraw up to $10,000 without incurring the 10% penalty. However, that $10,000 is still subject to state and federal income taxes.

Find ways to increase your income instead of using 401k withdrawals for your home purchase

If your employer does not offer 401 loans, they may still offer a 401 withdrawal. For people under the age of 59½, a “hardship” withdrawal or early withdrawal from your 401 is allowed under special circumstances, which are on the IRS Hardship Distributions page. Using your 410 for a down payment on a principal residence is classified as a hardship withdrawal. By opting to use a hardship withdrawal, you will have to pay the 10% early withdrawal penalty, and this amount will be considered taxable income. Generally, these exceptions are difficult to qualify for, so a 401 loan is usually better. Deciding whether it is a good idea to use your 401k to buy a house, you’ll likely want to borrow rather than withdraw money.

USDA mortgage rates are subsidized, and mortgage insurance rates are reduced. USDA loans are best for low- and moderate-income home buyers in suburban and rural locales. The government backs multiple low- and no-downpayment mortgage loans for first-time buyers, and the typical first-time home buyer doesn’t put twenty percent down. In the 1980s and 1990s, first-time home buyers used 401 plans to help buy homes because low- and no-downpayment mortgages were scarce. The employee is not obligated to repay or replace the cash withdrawn from the 401 account, but the IRS will recapture 10% of the amount withdrawn as part of the year’s federal tax filing. Money withdrawn may also count the withdrawal as taxable income.

If you need $25,000, you can simply take out a loan for $25,000 (assuming you have at least $50,000 in the account). Depending on the specifics of your account, you may also be eligible to take out a home loan of up to $50,000 against your 401K. Twin Cities Habitat for Humanity is an Equal Opportunity housing agency and Equal Opportunity Affirmative Action employer. You could own a home you love with a mortgage you can afford. Mortgage.info is your information portal for all things home, mortgage, and refinancing.

Employers can also make matching 401 contributions, which can translate into a more significant investment bump than a traditional IRA. Kira is a longtime blogger and serial entrepreneur who enjoys gardening, garage sales, and finding stray animals. She lives in Columbus, Ohio, where football is a distinct season, and by day runs a research study for people with multiple sclerosis. She hopes that the MoneyCrashers team can help you achieve your goals and live a great life.

Ask an accountant about the tax implications of withdrawing money from your 401 to make a down payment or purchase a home. By 1981, the IRS changed its rules so employers could fund retirement plans, and today, more than half of U.S. workers participate in an employee-sponsored 401 retirement plan. Home buyers can use their 401 retirement funds to make a downpayment on a home, but they shouldn’t.

Certain Roth IRA withdrawals can be made tax and penalty free. Qualified homebuyers can also seek financial help from down payment assistance programs and other low- or no-interest plans. Withdrawals from a 401 should not be made before the account holder turns 59½, or before they turn 55 and have left or lost their job. Early withdrawals incur a 10% early withdrawal penalty on the amount of money being taken out of the account. This amount also immediately becomes subject to income tax, since it’s no longer in the protected retirement savings account.

401 allows the account owner to withdraw the money, but it may have an early withdrawal penalty of 10% if withdrawn prematurely. You can take out a 401 loan for the lesser of half your vested balance or $10,000, whichever is more, or $50,000. You will incur interest that will be paid to your account, and you will not be able to make contributions until the loan is repaid. You can avoid penalties in certain situations, such as if your withdrawal is classified as a hardship withdrawal. You can use 401 funds to buy a house by either taking a loan from or withdrawing money from the account. But he finds that they don’t generally understand the rules, and they find it frustrating that they have money that they need but can’t access.

You can connect with her on her blog Adventurous Adulting. Our free course on buying your first home can help you with each step along the way. Take advantage of our free step-by-step side hustle guide. The other big downside to using your 401k funds to cover a down payment is the lost opportunity to grow your funds. When your funds are safely tucked away in your 401k, it has a few things going in the right direction.

Online Investments

Even if you’re short on cash and facing hardship, there are other options you might want to consider before tapping into your 401 account to cover the down payment on a house. It doesn’t count toward your debt-to-income ratio, and it won’t be counted by credit bureaus. So, taking a 401 loan won’t hurt your credit score and won’t affect your odds of qualifying for a mortgage.

No comments:

Post a Comment